Accidents happen in a flash — a fall, a crash, a sudden illness — and in moments, lives change. I used to think I was covered, until I dug into the fine print and realized my policy didn’t match the risks I actually face. The accident insurance market is booming, but not all plans are built the same. After researching dozens of options and comparing real-world claims data, I uncovered gaps most people overlook. This isn’t just about paying premiums — it’s about understanding what you’re really buying. What seemed like a simple safety net turned out to be full of limitations, assumptions, and silent exclusions that could leave families exposed when they need protection most.

The Hidden Reality Behind Accident Insurance Demand

In recent years, consumer interest in accident insurance has grown significantly, driven by evolving lifestyles and increasing awareness of financial vulnerability. More people are recognizing that a sudden injury can disrupt not only health but also income, daily routines, and long-term financial stability. The rise of remote work, for example, has introduced new types of household risks — from ergonomic injuries due to makeshift desks to slips in home environments not designed for full-time occupancy. At the same time, outdoor recreation has surged in popularity, with hiking, cycling, and adventure travel becoming common weekend activities. These shifts have changed how individuals perceive risk, moving accident coverage from a secondary consideration to a central piece of personal financial planning.

Another powerful driver is the rising cost of medical care. Even in countries with public healthcare systems, accident-related treatments often involve out-of-pocket expenses for rehabilitation, specialized equipment, or extended recovery support. Private insurance helps bridge these gaps, but many assume their existing health or employer-provided policies offer comprehensive protection. In reality, standard health plans may not cover non-medical costs such as lost wages, transportation to therapy, or home modifications after an injury. Accident insurance fills this space by offering lump-sum payouts or targeted benefits when an unexpected event occurs, giving families breathing room during difficult transitions.

Additionally, economic uncertainty has heightened sensitivity to financial shocks. With inflation affecting household budgets and job markets remaining unpredictable, people are seeking ways to reduce exposure to sudden expenses. Accident insurance offers a relatively low-cost way to gain peace of mind, especially for families without large emergency funds. This growing demand is reflected in market trends: global accident and health insurance premiums have risen steadily over the past decade, with particularly strong growth in urban centers where fast-paced living increases the likelihood of incidents. As lifestyles evolve, so too must the tools we use to protect ourselves — and accident insurance is no longer just an add-on, but a strategic component of modern financial resilience.

Mapping the Current Market Landscape

The accident insurance market today is more diverse than ever, shaped by both long-standing insurers and new digital players entering the space. Traditional providers — including well-known life and health insurance companies — continue to dominate in terms of market share, offering bundled packages that combine accident coverage with other protections. These established firms benefit from brand recognition, extensive agent networks, and regulatory compliance frameworks that inspire trust. However, they sometimes lag in innovation, with slower claims processing, rigid policy structures, and limited customization options. Their pricing models often rely on broad risk categories rather than individual behavior, which can result in higher premiums for low-risk customers.

In contrast, digital-first insurers and insurtech startups are reshaping expectations around accessibility and user experience. These companies leverage mobile apps, automated underwriting, and real-time data to deliver faster sign-ups and quicker claim settlements. Some operate entirely online, reducing overhead costs and passing savings to consumers. They also tend to emphasize transparency, presenting policy details in plain language and using interactive tools to help users understand their coverage. For instance, several platforms now offer instant quotes based on lifestyle inputs, allowing customers to see how different activities or occupations affect their rates before committing.

Regionally, there are notable differences in how accident insurance is structured and adopted. In high-income countries, coverage is often integrated into broader health or employment benefits, with individuals adding supplemental policies for extra protection. In emerging economies, standalone accident insurance is more common, sometimes promoted through microinsurance programs that make coverage affordable for lower-income households. These plans typically offer fixed payouts for specific events — such as fractures or hospitalization — and are distributed via mobile networks or community organizations. While benefit amounts may be smaller, the accessibility and simplicity of these products have made them vital tools for financial inclusion.

Transparency, pricing fairness, and ease of claims are now key competitive factors across markets. Consumers increasingly expect clear communication about what is covered, how premiums are calculated, and how quickly they can access funds after an incident. Providers that fail to meet these expectations risk losing trust and market share. At the same time, regulatory bodies in various countries are tightening oversight to prevent misleading sales practices and ensure that policies deliver on their promises. As competition intensifies, the industry is moving toward greater accountability — a shift that ultimately benefits consumers seeking reliable, value-driven protection.

What Standard Policies Actually Cover (and Where They Fall Short)

Most accident insurance policies include a core set of benefits designed to address immediate financial needs following an injury. Common features include lump-sum payments for accidental death or dismemberment, reimbursement for emergency medical treatment, and compensation for hospital stays. Some plans also cover surgery costs, ambulance services, and short-term disability resulting from an accident. These benefits can provide crucial support, especially when injuries lead to lost income or unexpected expenses. For example, a parent who suffers a broken leg may face weeks off work and require home care assistance — costs that standard health insurance may not fully cover. In such cases, an accident policy can help maintain financial stability during recovery.

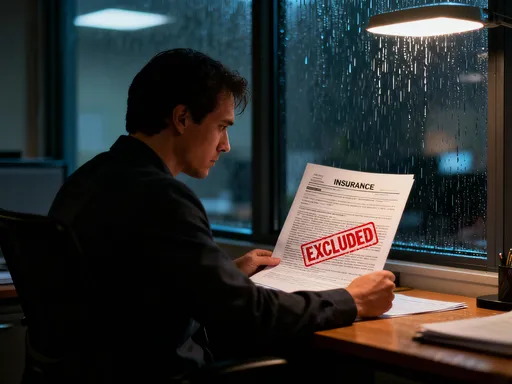

However, the limitations of standard policies often become apparent only after a claim is filed. One major issue is the presence of exclusions — conditions or situations under which no payout will be made. Many policies exclude injuries related to pre-existing medical conditions, even if the accident itself was unforeseen. Others do not cover incidents that occur during high-risk activities such as skydiving, motor racing, or certain professional sports. Even seemingly routine behaviors like riding a motorcycle or participating in organized fitness challenges may void coverage if not explicitly declared. These exclusions are typically buried in dense legal language, making it easy for consumers to overlook them until it’s too late.

Another common gap involves mental health impacts. While physical injuries are usually addressed, the psychological consequences of an accident — such as anxiety, PTSD, or depression — are rarely covered under standard accident plans. Yet these conditions can be just as debilitating and costly, requiring therapy, medication, and time away from work. Similarly, long-term rehabilitation services like physical therapy or occupational training are often capped or excluded, leaving families to absorb ongoing expenses. There is also inconsistency in how policies define “accident” — some require the event to be sudden and external, which may disqualify claims related to gradual strain or overexertion, even if the injury feels acute.

Real-world claim scenarios highlight how small wording differences can have major financial consequences. Consider two individuals who suffer falls at home: one lands on a hard floor and fractures a wrist, while the other slips in the shower and develops a back injury over time. The first may qualify for benefits, but the second might be denied if the policy requires immediate trauma from a single event. Likewise, a cyclist hit by a car may receive full coverage, but a runner who trips on uneven pavement might not — depending on whether the policy considers the injury “externally caused.” These nuances underscore the importance of reading policy documents carefully and asking detailed questions before purchasing. Coverage is not universal, and assumptions can lead to costly surprises when protection is needed most.

Why One-Size-Fits-All Doesn’t Work Anymore

The traditional model of accident insurance — offering standardized plans to broad customer groups — is increasingly out of step with modern lifestyles. People’s daily routines, occupations, and risk profiles vary widely, yet many policies treat them as interchangeable. A gig economy driver faces different hazards than an office worker, just as a frequent traveler encounters more exposure than someone with a sedentary routine. Recognizing this mismatch, forward-thinking insurers are shifting toward personalized and modular coverage models that adapt to individual needs. These approaches allow policyholders to tailor their protection based on actual risk factors, ensuring better alignment between premium costs and real-world benefits.

Occupation plays a significant role in determining risk exposure. Construction workers, delivery personnel, and healthcare providers, for example, are more likely to experience workplace injuries than those in desk-based roles. Yet many standard policies either charge higher premiums across the board or exclude certain jobs altogether. Newer solutions address this by offering tiered pricing or optional add-ons for high-activity professions. Similarly, age and lifestyle habits influence risk — younger adults may engage in more physical activities, while older individuals may be more prone to falls. Instead of applying blanket restrictions, customizable plans can adjust coverage levels accordingly, providing greater flexibility and relevance.

Modular insurance designs enable users to build their own protection packages by selecting specific benefits. For instance, a cyclist might add enhanced coverage for fractures and emergency transport, while a remote worker could prioritize benefits related to ergonomic injuries or home-based accidents. This à la carte approach improves value by eliminating unnecessary components and focusing on what matters most to the individual. Some providers even allow policyholders to adjust their coverage mid-term, reflecting changes in routine or seasonal activities like skiing or gardening.

Equally transformative is the rise of on-demand insurance platforms. These digital services let users activate coverage only when needed — for example, purchasing temporary protection before a hiking trip or renting sports equipment. Using smartphone apps, customers can initiate policies in minutes, often paying only for the days they require protection. This model appeals to cost-conscious consumers who want flexibility without long-term commitments. It also reduces waste by avoiding year-round premiums for risks that occur infrequently. As technology enables more precise risk assessment and instant policy management, the industry is moving away from rigid, one-size-fits-all products toward dynamic, user-centered solutions that better reflect how people live today.

Smart Risk Control: Balancing Cost and Coverage

Selecting the right accident insurance plan requires more than comparing price tags — it demands a thoughtful evaluation of value, risk exposure, and long-term financial impact. A low-premium policy may seem attractive initially, but if it lacks essential benefits or imposes strict limitations, it could leave significant gaps in protection. Conversely, a more expensive plan might offer comprehensive coverage that justifies its cost over time. The key is to assess each option using a balanced framework that considers payout structures, waiting periods, renewal terms, and overall alignment with personal circumstances.

One effective strategy is to analyze the benefit-to-premium ratio. This involves reviewing how much the policy pays out for common scenarios — such as hospitalization, surgery, or permanent disability — relative to the annual cost. A plan that offers a $10,000 payout for a $200 premium may appear favorable, but only if the conditions for receiving that payout are realistic and clearly defined. It’s equally important to examine waiting periods, which determine how soon benefits become available after an incident. Some policies impose delays of several days or weeks, which could create cash flow challenges during early recovery. Shorter waiting periods typically come with higher premiums, so consumers must decide whether immediate access to funds is worth the added cost.

Renewal terms are another critical factor. Many policies are renewable annually, but insurers may adjust premiums based on claims history, age, or market conditions. Some plans guarantee level rates for a set period, while others allow rate increases without prior notice. Understanding these terms helps avoid unexpected cost spikes down the line. Additionally, checking whether a policy is guaranteed renewable — meaning it cannot be canceled as long as premiums are paid — provides greater long-term security, especially for individuals with chronic conditions or past claims.

To improve affordability without sacrificing protection, several practical strategies exist. Bundling accident insurance with other policies, such as health or life insurance, often results in discounts and simplified administration. Choosing a higher deductible — the amount the policyholder pays before benefits kick in — can also reduce premiums, provided the individual has sufficient savings to cover initial expenses. For families, group plans through employers or associations may offer lower rates than individual purchases. Ultimately, the goal is not to minimize cost at all costs, but to achieve long-term cost efficiency by selecting a plan that delivers meaningful protection when it’s needed most.

The Role of Technology in Claims and Trust

Technology is transforming the accident insurance experience, particularly in how claims are filed, processed, and verified. In the past, submitting a claim often involved mailing paper forms, waiting weeks for approval, and navigating unclear communication. Today, digital platforms enable mobile claims filing with photo uploads, electronic signatures, and real-time status tracking. These improvements reduce delays and increase transparency, helping policyholders access funds faster during stressful times. Some insurers use AI-powered systems to assess claims automatically, flagging inconsistencies or missing documents instantly, which speeds up resolution and reduces administrative errors.

Blockchain technology is also being explored to enhance trust and security in claims processing. By creating immutable records of policy terms and claim submissions, blockchain can prevent tampering and ensure data integrity. This is especially valuable in cross-border cases or situations where multiple parties are involved, such as third-party administrators or healthcare providers. While still in early adoption phases, blockchain-based verification has the potential to reduce fraud and build stronger consumer confidence in the fairness of outcomes.

Personalization is another area where technology is making a difference. Some insurers now integrate wearable devices or telematics to monitor behavior and adjust premiums accordingly. For example, a driver who uses a connected car device demonstrating safe habits may qualify for lower rates on an accident policy. Similarly, fitness tracker data showing regular activity and healthy routines could signal lower risk, leading to preferential pricing. These innovations move away from generalized risk pools toward more individualized assessments, rewarding responsible behavior and improving pricing accuracy.

Despite these advances, concerns remain about data privacy and algorithmic fairness. Consumers rightly worry about how their personal information is collected, stored, and used in underwriting decisions. Insurers must prioritize strong cybersecurity measures and clear consent protocols to maintain trust. They should also ensure that automated systems do not introduce bias — for example, by disproportionately penalizing certain demographics based on incomplete or skewed data. When implemented responsibly, technology can enhance both efficiency and equity in the insurance process, creating a more responsive and trustworthy system for everyone.

Building a Future-Proof Accident Protection Plan

Given the rapid changes in lifestyle, work patterns, and insurance technology, a static approach to accident coverage is no longer sufficient. A future-proof protection plan requires ongoing attention, adaptability, and informed decision-making. Rather than treating insurance as a one-time purchase, consumers should view it as a dynamic part of their financial strategy — one that evolves alongside life changes such as career shifts, family growth, or relocation. Regular reviews, ideally once a year or after major milestones, ensure that coverage remains aligned with current needs and risks.

An effective strategy combines the reliability of traditional policies with the flexibility of emerging models. For instance, maintaining a core accident plan with broad coverage provides a stable foundation, while supplementing it with on-demand or modular options allows for targeted protection during high-risk periods. This hybrid approach balances consistency with responsiveness, offering both security and adaptability. It also supports smarter budgeting, as individuals can scale coverage up or down based on immediate requirements rather than paying for unused benefits.

Education plays a crucial role in building long-term resilience. Understanding policy terms, recognizing common exclusions, and knowing how to compare plans empowers consumers to make confident choices. Resources such as independent review platforms, financial advisors, and insurer-provided tools can aid in this process. Asking the right questions — such as “What triggers a payout?” “Are mental health impacts included?” and “Can I adjust coverage mid-term?” — helps uncover hidden limitations and identify truly suitable options.

Ultimately, the goal is to move beyond passive coverage toward active financial stewardship. Accident insurance should not be a forgotten line item on a monthly bill, but a deliberate choice rooted in awareness and intention. In a market shaped by innovation and increasing complexity, informed decisions are the strongest form of protection. By staying engaged, adapting to change, and prioritizing clarity over convenience, individuals and families can build a safety net that truly supports them — not just today, but in whatever future lies ahead.